Erik Caseres - Coldwell Banker Commercial CBS

Will 2025 Finally Bring a CRE Comeback—Or Just More Uncertainty?

What Investors Need to Know About the Market’s Uneven Recovery and Emerging Opportunities

BIG SKY BIZ JOURNAL

Erik Caseres

2/24/20254 min read

Will 2025 Finally Bring a CRE Comeback—Or Just More Uncertainty?

Commercial real estate (CRE) faced headwinds in early 2024 due to delayed interest rate cuts, election uncertainty, inflation, and tighter lending standards. However, as the Federal Reserve executed two rate cuts and post-election clarity set in, investors re-engaged in the market, anticipating a more business-friendly environment in 2025. While we do not expect a sharp rebound, modest improvements are likely as fundamentals stabilize, leading to better pricing and demand. That said, recovery will be uneven across geographies and property types, with cap rates compressing selectively in key markets and sectors.

Macroeconomic Landscape

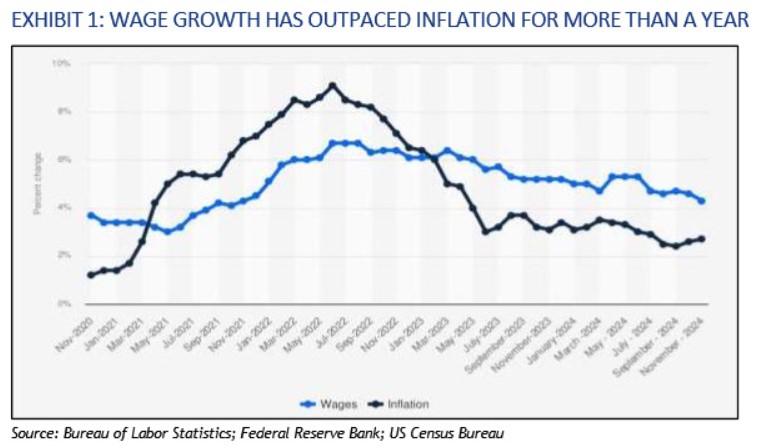

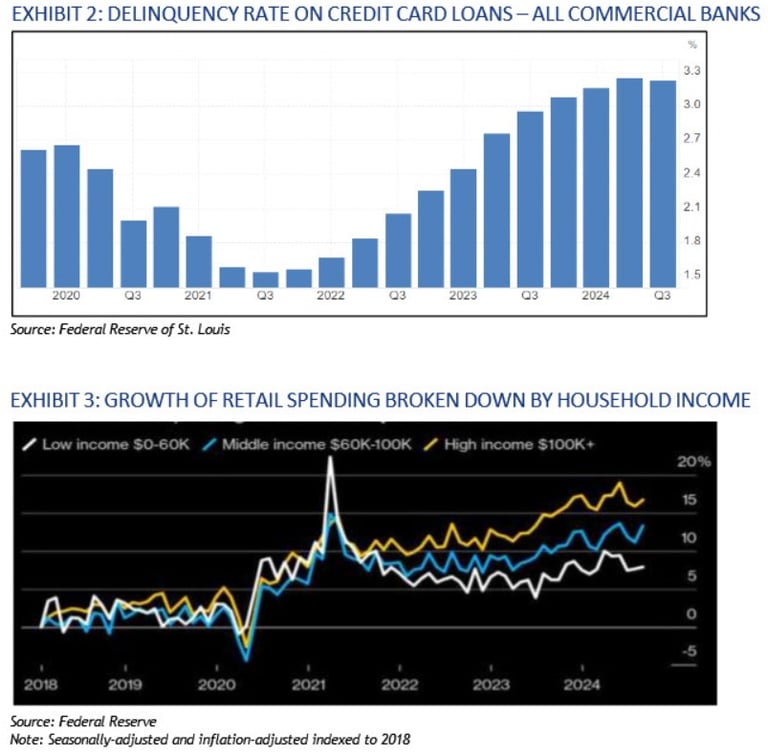

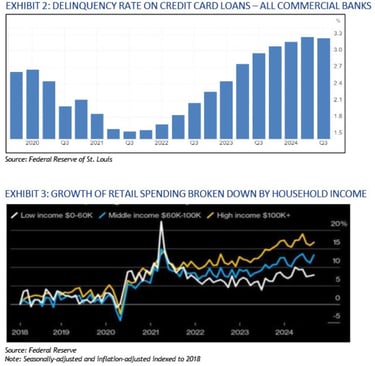

The U.S. economy exceeded expectations in 2024, driven by strong consumer spending, low unemployment, and easing inflation despite high borrowing costs. Wage growth continued to outpace inflation (Exhibit 1), and household wealth reached record highs, with net worth rising by $4.8 trillion and equity holdings increasing by $3.8 trillion in Q3 2024 (source: Federal Reserve). However, many consumers have depleted their pandemic savings and are increasingly reliant on credit cards, leading to financial strain (Exhibit 2). Looking ahead, economic growth will be led by higher-income earners, while middle- and lower-income consumers scale back spending (Exhibit 3).

Market Dynamics: A Closer Look at CRE Recovery

With only two Fed rate cuts projected for 2025—down from the four originally expected—CRE’s recovery will be steady but uneven. Market activity remains driven by well-capitalized buyers, 1031 exchanges, and private equity. Institutional asset sales have seen major discounts, while mid-sized properties held by family businesses are seeing price reductions of 10-20%. In contrast, smaller buildings are fetching premiums due to strong demand from local investors.

Buyers range from international investors seeking trophy buildings to local private investors acquiring small properties. Developers are securing land for future construction, while companies needing relocation are accepting high construction costs. In markets where cap rates do not justify current pricing, sellers are offering financing to close deals.

Key Trends Across Property Sectors

Retail:

Strong tenant demand due to low vacancies and robust consumer spending.

Competitive leasing environment with rising rents, especially for fast casual, grocery, and value retail.

Limited retail supply is driving new development, particularly in high-income areas.

Strip centers, grocery-anchored properties, and drive-thrus remain top investor picks.

Industrial:

Large industrial spaces (100,000+ SF) are struggling with higher vacancy rates due to last year’s supply surge.

Smaller industrial spaces (under 30,000 SF) remain in high demand, commanding premium rents.

Multi-tenant warehouses and subdividing large spaces present opportunities for higher rental yields.

Office:

Downtown office buildings continue to struggle with high vacancies (20-30%).

Landlords are signing shorter leases, offering turnkey spaces, and cutting rates by 20-30%.

Medical offices and suburban office spaces (1,000-4,000 SF) are seeing strong demand.

Conversions of outdated office buildings to medical, mixed-use, and self-storage are on the rise.

Higher-end office space in select markets is seeing renewed interest, particularly in the Sun Belt and suburban areas.

Multifamily:

Oversupply and high costs have slowed multifamily development, shifting focus to single-family communities.

Class A assets in select markets (e.g., Phoenix, Las Vegas, Boston) remain attractive due to high-income migration.

Multifamily permit activity is expected to decline significantly in 2025, tightening future supply and potentially supporting rent growth.

Workforce housing and build-to-rent communities are emerging as strong investment opportunities.

Hospitality:

Travel demand remains strong, with higher occupancy rates in leisure-driven markets.

Select-service hotels and extended-stay properties continue to outperform.

Urban hotels are experiencing uneven recovery, with business travel still lagging pre-pandemic levels.

Financing and Lending Trends

Traditional banks remain hesitant to fund office and multifamily deals, favoring medical office and owner-user properties. Lending conditions remain strict, with banks requiring 40-50% equity, at least 50% occupancy, and limited cash-out refinancing options. As a result, CRE transactions are increasingly funded through:

Regional and local banks, offering loans in the low-7% range with 20-30% down.

Seller financing, as debt-free owners offer terms to achieve higher sale prices.

Credit unions, which significantly increased their CRE loan holdings in 2024, growing at four times the national average.

Private equity, filling gaps in markets where traditional lenders remain cautious.

Debt funds, stepping in to provide bridge loans as banks pull back on riskier assets.

Outlook for 2025

While optimism is returning, the pace of recovery will vary by market and asset class. High-growth regions with new development projects—such as HQs, hospitals, and sports arenas—are experiencing stronger investor confidence. In contrast, office and industrial sectors remain volatile, requiring strategic repositioning and creative financing solutions.

Cap rates have risen by 50-100 bps over the past year, but well-located Class A properties are stabilizing, while Class B and C assets may see further declines. Distressed sales have been limited in 2024 but are expected to increase as loan maturities rise in 2025.

Conclusion

With a more business-friendly climate expected in 2025, CRE investors are cautiously optimistic. Cash transactions, 1031 exchanges, and alternative lending solutions will continue driving the market. While challenges remain—particularly in office and select industrial submarkets—the fundamentals are aligning for a gradual, sector-specific recovery in the coming year.

Expertise

Specializing in business brokerage services & commercial real estate transactions.

Contact

Inquire

erik@cbcmontana.com

© 2024. All rights reserved.